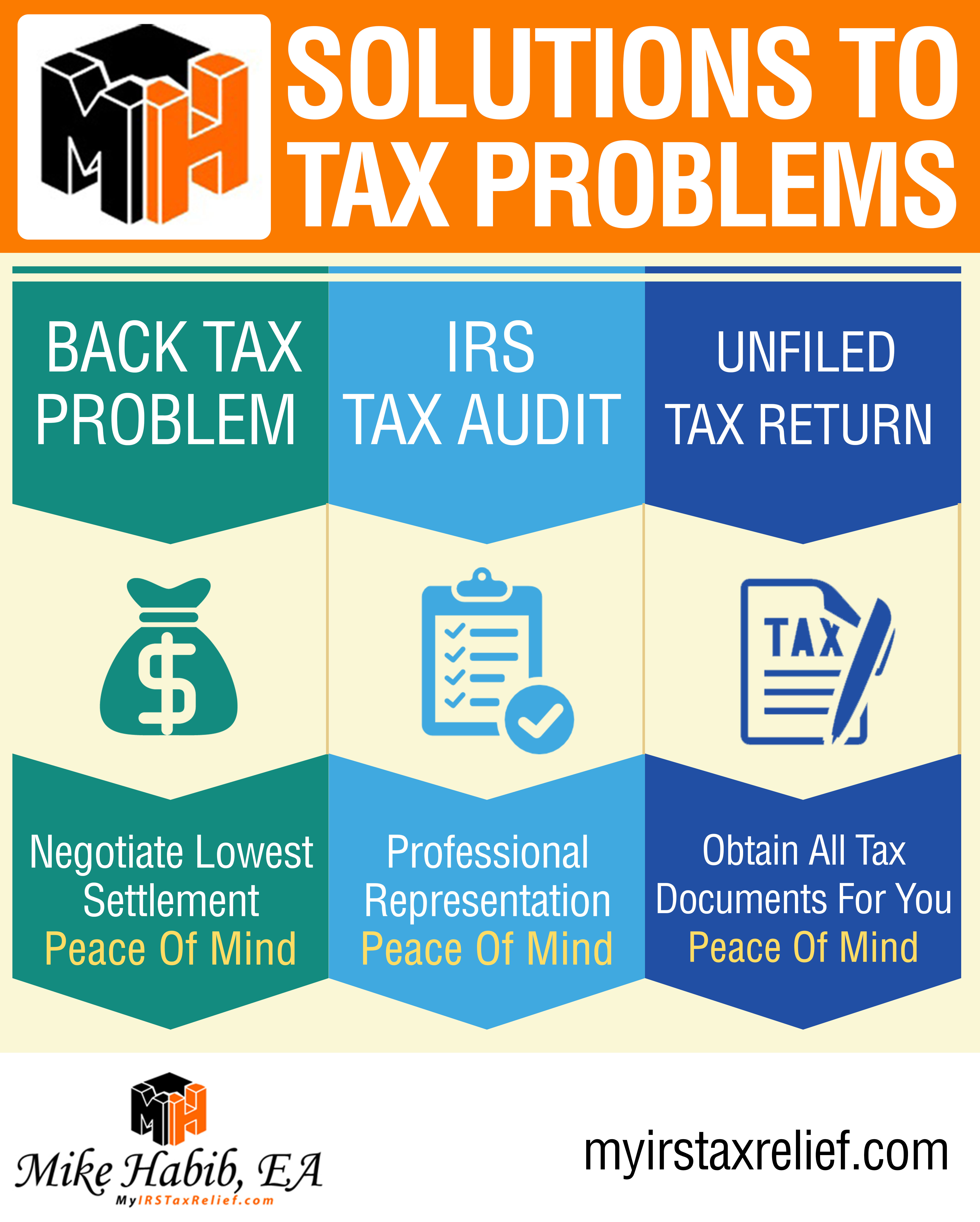

Tax Problem Resolution infographic by Mike Habib EA, Back taxes Help, IRS Audit Help, Unfiled Tax Returns Help

Tax Problem Resolution infographic by Mike Habib EA

Calling on taxpayers facing back tax problems, taxpayers being audited by the IRS or the state, taxpayers with delinquent and unfiled tax returns, releasing tax levies, tax liens and businesses facing 941 payroll tax problems. We can resolve your tax problem and offer you peace of mind. Call us today at 877-788-2937.