Employment Tax Problem? Get resolution today!

Los Angeles – San Francisco – New York – Chicago – Denver – Houston – Atlanta – Miami

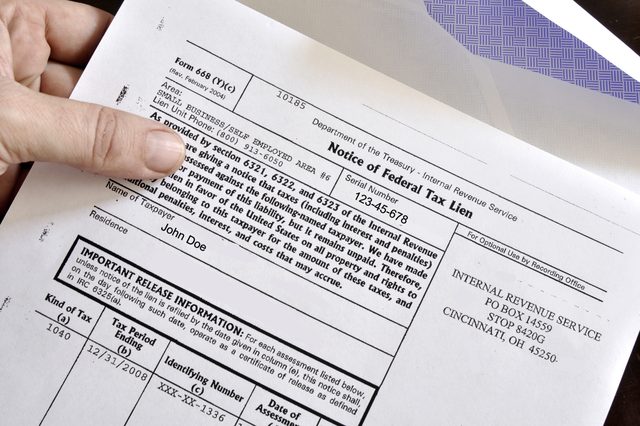

Employment 940/941 Taxes

If you have your own business, there is plenty going on all the time. In addition to taking care of your customers, you have to take care of your employees. Payroll can be very difficult with the many scenarios, and that can lead to an employment tax problem. Don’t feel like you are alone though as 941 payroll tax problems are extremely common when it comes to the IRS and what they have to look into.

Get a free evaluation of your case at 877-788-2937.